August 18, 2021 | Business Strategy

by José A. Miranda, Lillian Symonds

Data management is a game of imbalances in which the winner is always the same.

The volume of advertising business at stake is increasing, and the big technology companies are leading the way.

Digital advertising investment has been increasing over the last few years with growth above double digits in almost every market, which has led to capture around 60% of total spending globally reaching around $478.2Bn(*) USD by the end of 2021, estimating a market of $636.2Bn(*) USD by 2024.

As can be seen, the volume of business at stake is increasing, which leads us to a non-zero-sum game environment; something which, in principle, is positive, since it opens up new market options for all players. But we must not forget that it is the big technology companies that are leading the way forward, and where, obviously, they always win.

Undoubtedly, once open TV is digitized and the transformation of the components of out-of-home advertising and other media is maximized over the next few years, we will no longer talk about digital advertising investment as such.

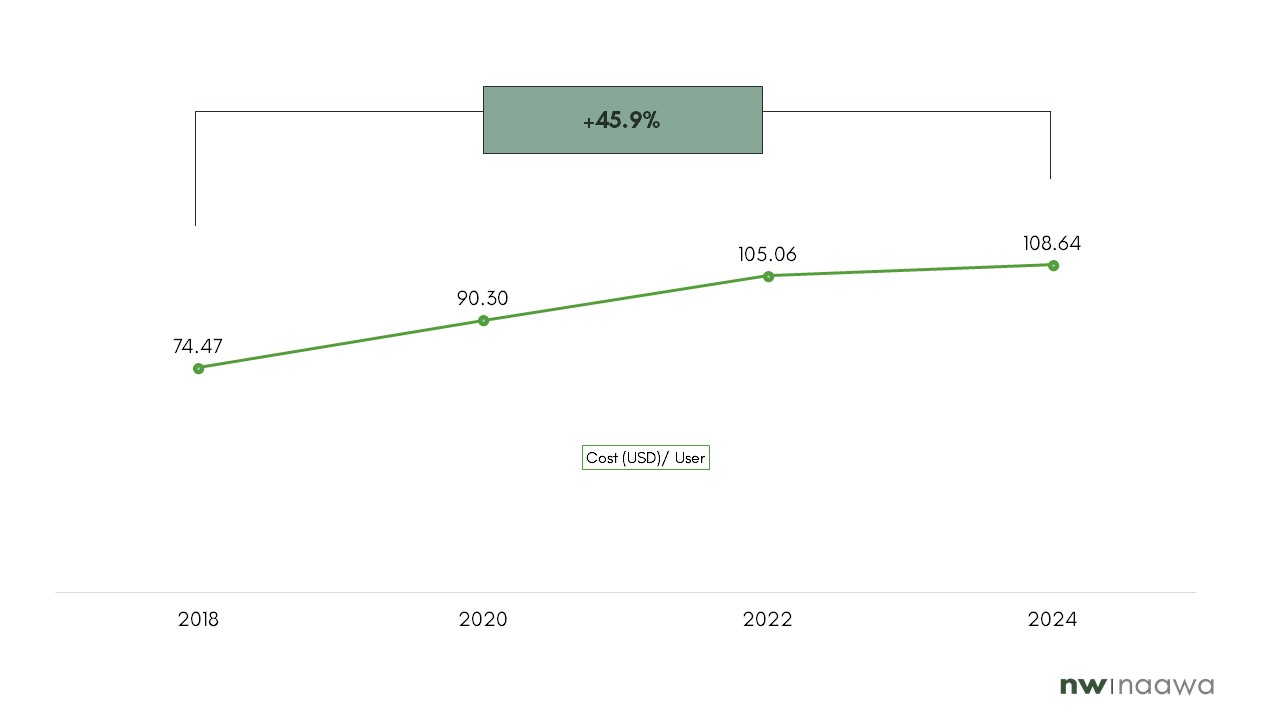

And even if the advertising market is growing, the digital contact cost per user will increase by +45.9% from 2018 to 2024; in other words, it will be necessary to increase the control and efficiency of advertising management over the next few

years.

Source: GroupM, Statista, eMarketer

In addition, authorities increasingly require greater protection of users in terms of privacy, so they will try to implement certain regulations in terms of security and transparency, which will directly affect the management of the huge advertising market previously mentioned.

The focus of this user privacy defense is mainly directed towards blocking or deleting so-called third-party cookies from browsers. Simply put, these cookies are identifiers that allow advertisers (and other actors) to track users behavior in the different websites, which in turn, allows them to segment them almost “individually”, reaching a potential hyper-segmentation, which will be used by companies to offer personalized products and services based on the interests of users.

In other words, they are massive databases containing the browsing behavior of users. These users are defined through identifiers and can be further refined when crossed with databases of another nature which, in turn, contain unique identifiers of individuals (login, email, etc…).

Among the technological solutions that are being introduced in the market by companies, there are different approaches on how to deal with the way to strengthen user privacy.

Thus, Google released a few months ago the news about the elimination of these cookies from its Chrome browser (which market share is globally almost 70%) by 2023, which will not be replaced by other similar technology, but by a new one that will strengthen the privacy of users in their navigation, which certainly seems positive.

In this sense, Google proposes The Privacy Sandbox, an open and collaborative development framework, where different solutions such as FLEDGE or FLoC converge, which are based on generating cohorts (or groups) of individuals that have similar behavior, but do not identify the users that make up these groups individually. In this way, advertisers will be able to target groups of behavior, not individuals.

Meanwhile, other browsers such as Firefox and Safari also offer the option to block third-party cookies. And, on the other hand, companies that manage the buying and selling of advertising inventory informed the market about their alternative solutions to stop tracking third-party cookies.

For example, The Trade Desk launched the Unified ID 2.0 solution, which allows the encryption of data that identifies users, such as e-mail, also under a collaborative open development environment.

All of this current evolution entails the collaboration and involvement of the regulatory bodies in the different markets to protect the privacy of users. And, while ” open collaborative ” environments are being promoted in this new market scenario, the potential business volume to be tapped is very clear and far too juicy.

Hence, the efforts of large technological organizations are focused on the creation of increasingly closed environments that enable maximum control of these huge databases containing user information and are what really allow these organizations to maximize the monetization of advertising revenues. And, creating and maintaining these active databases, with the highest quality, doesn’t come for free.

Because we must never forget that databases are generated for the sole purpose of using them. And the higher the quality of these databases, the more value they generate, and the better they can be monetized.

Therefore, it is highly likely that the increase in data quality will lead to an increase in management costs, which, in turn, will result in higher selling prices. And, where the big technology companies will continue to lead the way in the marketplace.

That’s really the big change that’s coming.

José A. Miranda is Managing Partner at Naawa, Lillian Symonds is Business Solutions Partner at Naawa.

Copyright © 2021 Naawa Consulting. All rights reserved.

Download the full article in PDF here:

“We want to become the best valued partner to our clients based on helping companies to lead sustainable growth by inspiring talented challenging minds.”